Case Studies

What we find

Every Lead2Cash engagement starts the same way. Before recommending software, restructuring teams, or changing processes, we model how the business actually moves from the first sales conversation to collected cash. What the model reveals is often not the problem the company thought it had. These case studies show what became visible once the revenue system was examined across companies in construction, manufacturing, professional services, facility services, SaaS, ecommerce, private equity, media, and fintech.

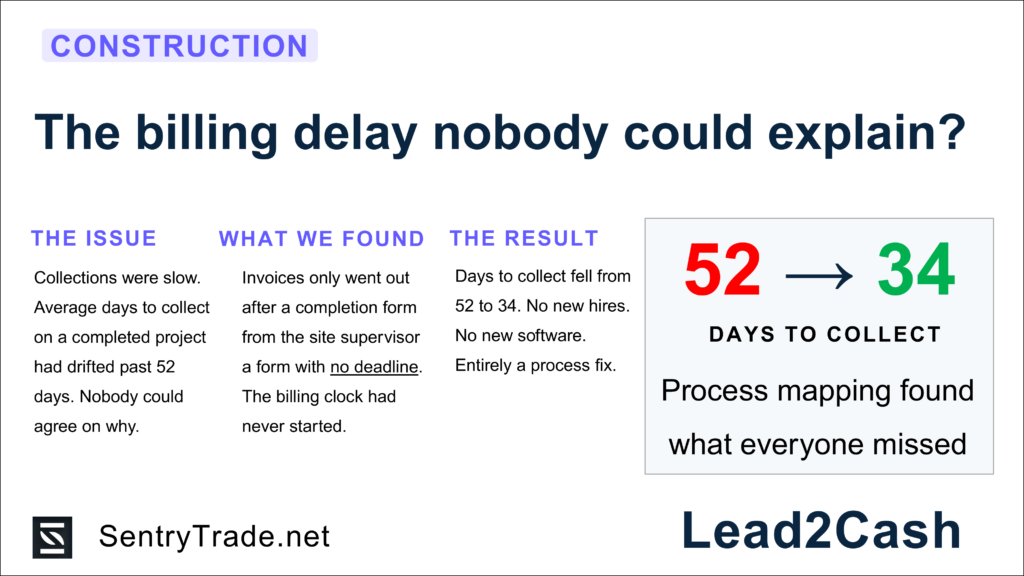

The billing delay nobody could explain

Industry: Commercial construction contractor

The problem: Collections were slowing and nobody could explain why. The owner suspected slow customers. The finance team suspected billing delays. Operations suspected contract confusion. Average collection time had drifted past 52 days, even though project backlog remained strong.

What Lead2Cash revealed: The problem was not collections. Invoices were triggered only after a signed project completion form arrived from the site supervisor. That form typically arrived 6 to 11 days after the work was finished. Each regional team also used a different definition of what “complete” meant before submitting the form. The billing clock was starting late.

What changed: Billing was triggered at practical completion, not when internal paperwork happened to arrive. Invoices were required to be issued within 24 hours of completion.

Result: Average collection time dropped from 52 days to 34 days within one quarter. No new hires. No new software.

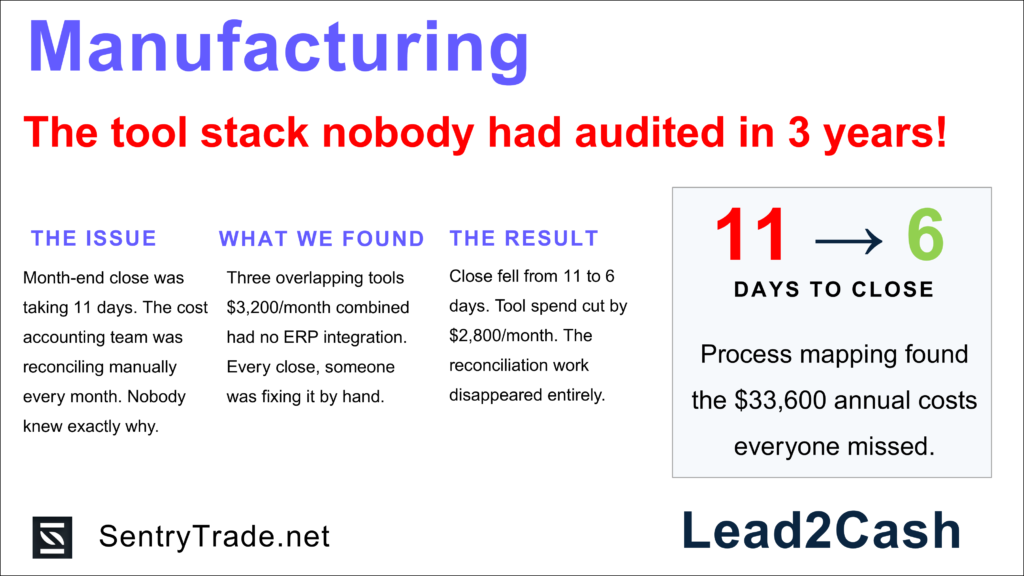

The tool stack that nobody had audited in 3 years

Industry: Contract manufacturing

The problem: Operations felt slow and fragmented. Finance had a different concern: the monthly close required 11 days and involved heavy reconciliation between multiple systems. No one had a clear picture of how many tools were actually involved in the revenue process.

What Lead2Cash revealed: Four separate tools were handling overlapping functions in order management and job costing. Three of them were not integrated with the ERP. Manual reconciliation between systems was responsible for four days of the close process. The total cost of the revenue tool stack was $11,400 per month.

What changed: Three overlapping tools were consolidated into a single system integrated directly with the ERP. The manual reconciliation step was eliminated.

Result: Close reduced from 11 days to 6 days. Monthly tool spend dropped by $2,800. Two days of analyst reconciliation work disappeared entirely.

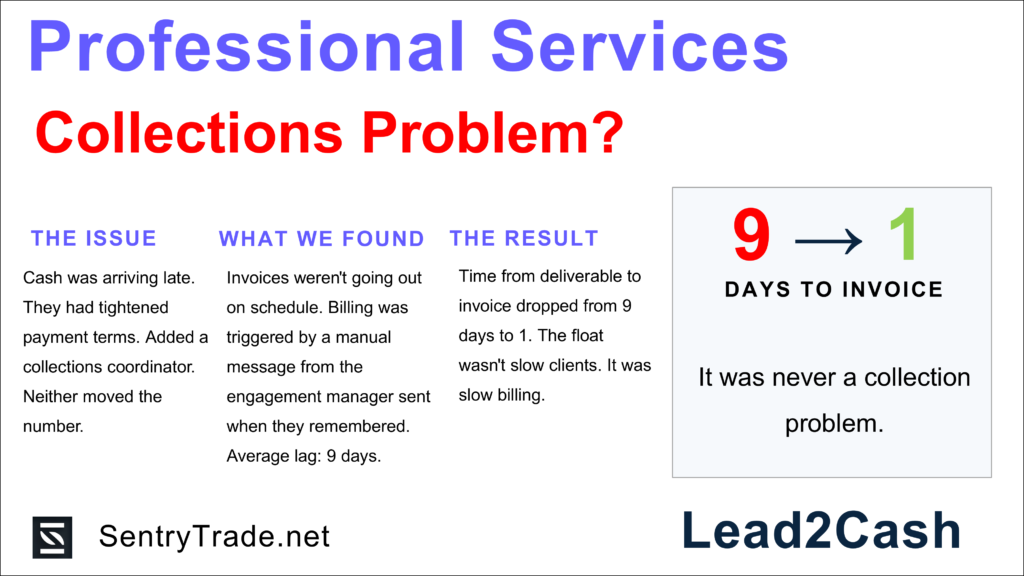

The firm that thought it had a collections problem

Industry: Management consulting firm

The problem: Invoices were going out, but cash was consistently arriving later than expected. The firm estimated it was carrying two to three weeks of unnecessary float. They tightened payment terms and added a collections coordinator. Neither helped.

What Lead2Cash revealed: Invoices were not being triggered consistently. Billing depended on engagement managers sending a completion notification, which averaged nine days after deliverables were submitted. The firm also had four engagement types, each with different informal billing practices.

What changed: A standardized billing trigger was implemented for all engagement types. Completion notifications were generated automatically from the project system rather than manually by engagement managers.

Result: Time from deliverable completion to invoice delivery dropped from nine days to one. Most of the “collections problem” disappeared.

The hidden cost of a growing headcount

Industry: Facility services company

The problem: Revenue had grown steadily, but profitability was compressing. Leadership believed fixed costs were increasing faster than revenue.

What Lead2Cash revealed: The total monthly labor cost associated with the revenue cycle was $187,000. Leadership had estimated it closer to $140,000. Several roles had gradually taken on billing and reporting work that was not visible in financial reporting. The billing cycle itself also introduced structural delay. For many contracts, services were delivered early in the month but invoiced at month end.

What changed: Billing triggers were moved closer to service delivery. Operational roles were restructured so non billable reporting work did not accumulate across multiple positions.

Result: Average time from service delivery to cash fell from 47 days to 31 days. Non billable labor costs dropped by $22,000 per month.

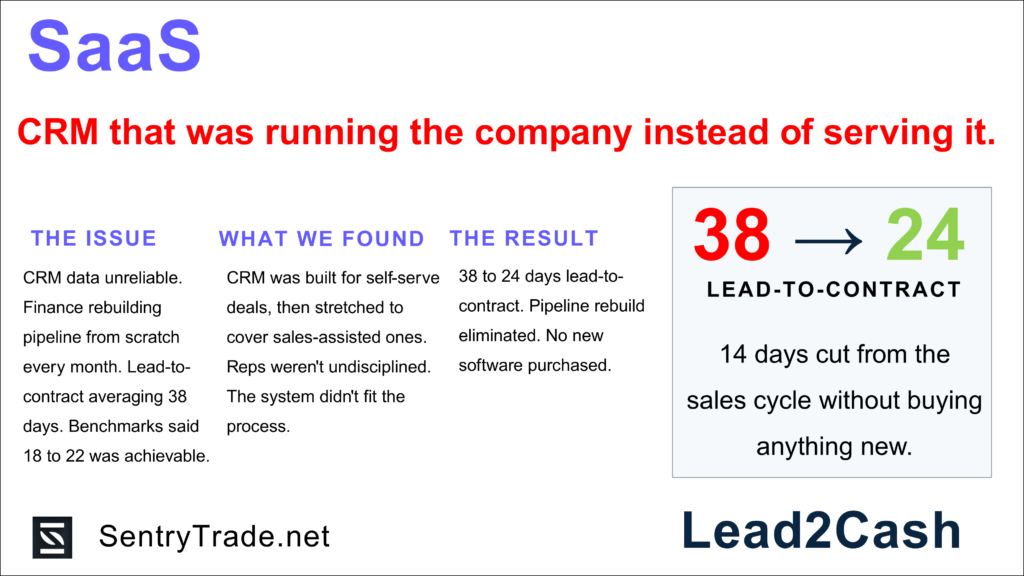

The CRM that was running the company instead of serving it

Industry: B2B SaaS company

The problem: The CRM was supposed to be the source of truth for the sales cycle. In practice, complex deals were tracked across spreadsheets, email threads, and external project systems. Sales cycle time averaged 38 days, well above industry benchmarks.

What Lead2Cash revealed: The sales process contained 11 steps before contract execution. Many had been added over time to address edge cases. The CRM was configured for a self serve motion and had been stretched to support a sales assisted motion. Sales teams created parallel tracking systems because the CRM structure no longer matched the actual process.

What changed: Two separate sales flows were modeled: self serve and sales assisted. The CRM was reconfigured to match the real process. Four unnecessary steps were eliminated.

Result: Average lead to contract time dropped from 38 days to 24 days. CRM pipeline data became reliable enough for finance forecasting.

Twenty thousand SKUs and no reliable cost picture

Industry: Consumer electronics ecommerce retailer

The problem: Finance could not produce reliable landed cost figures. Month end close took 14 days and often required post close adjustments.

What Lead2Cash revealed: Landed costs including freight and duties were being calculated manually in spreadsheets at month end. Three different employees were calculating adjustments using slightly different methods. The manual close process cost $31,000 per month in labor.

What changed: Cost components were passed directly from the warehouse system to the ERP. Manual spreadsheet adjustments were eliminated.

Result: Month end close dropped from 14 days to 7 days. Close related labor costs fell by $18,000 per month. Channel level margin reporting became reliable.

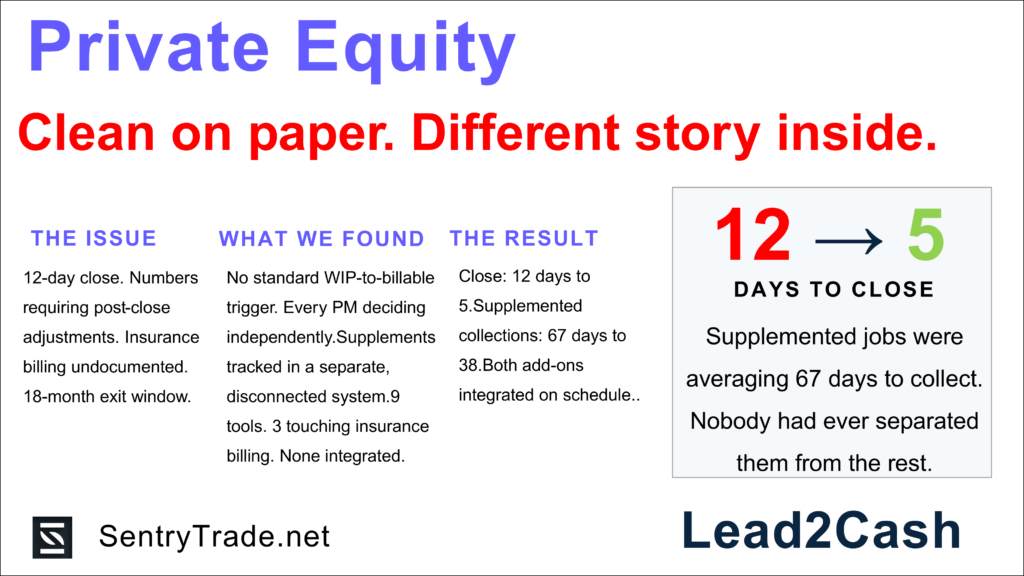

The acquisition that looked clean until the process was examined

Industry: Private equity backed restoration contractor

The problem: A newly acquired platform company had inconsistent project accounting and a 12 day close cycle. This was incompatible with the PE firm’s 18 month exit timeline.

What Lead2Cash revealed: Each project manager defined job completion differently. The work in progress balance was not a reliable financial figure. Insurance billing supplements were also tracked in a separate system. Supplemented jobs took 67 days to collect, compared to 31 days for standard jobs.

What changed: Completion triggers were standardized across project managers. Supplement tracking was integrated into the main project accounting platform.

Result: Close dropped from 12 days to 5 days. Supplemented job collections fell from 67 days to 38 days. The platform was stabilized ahead of the PE firm’s exit timeline.

The receivables that looked fine until the ownership changed

Industry: Digital media company

The problem: Thirty percent of receivables were either disputed or more than 90 days old. Cash stability became an urgent concern after an ownership transition.

What Lead2Cash revealed: Advertisers who had stopped spending were still active in the billing system. Collections followed the same process for healthy customers and inactive accounts. Subscription renewals were also delayed because one employee handled both renewals and billing disputes.

What changed: Advertiser offboarding rules were introduced. Renewal processing and billing disputes were separated into different workflows.

Result: Bad debt fell from 18% of revenue to under 4%. Collections stabilized within 60 days.

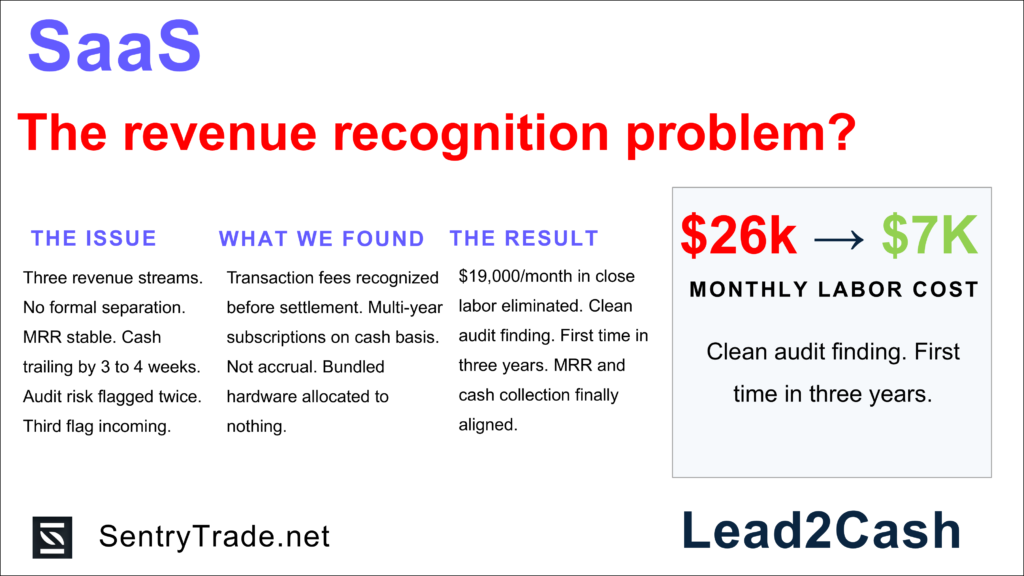

The revenue recognition problem inside a payment platform

Industry: Global retail SaaS and payment platform

The problem: Three revenue streams were being recognized through a combination of billing systems and manual spreadsheet adjustments. Auditors had flagged revenue recognition risk twice.

What Lead2Cash revealed: Transaction fees were recognized before settlement occurred. Subscription contracts were recognized on a cash basis rather than ratably. Bundled hardware and software contracts were not properly allocated. Manual adjustments during close cost $26,000 per month in labor.

What changed: Revenue recognition rules were rebuilt and embedded into the billing system. Transaction settlement lag was modeled directly rather than corrected manually.

Result: Manual close adjustments were eliminated. Audit risk was resolved. Monthly close effort dropped significantly.

Every one of these started the same way

Not with a product demo. Not with a consulting proposal. With a structured session documenting how the business actually worked. Once the system becomes visible, the improvements usually become obvious.

Start with visibility

Before buying new software. Before adding headcount. Before trying to fix collections, billing, or operations. See the system first.